By Khawar Azhar

Pakistan’s automobile industry is standing at one of the most decisive moments in its 40-year history. What began in the 1980s with Pak Suzuki’s basic 800cc CKD assemblies gradually evolved into a full-fledged manufacturing ecosystem — one that supports millions of livelihoods and billions of dollars in investment. But today, that same ecosystem finds itself under pressure from a policy direction that increasingly appears to favour imports over local production.

The New Challenge: Rising Used-Car Imports

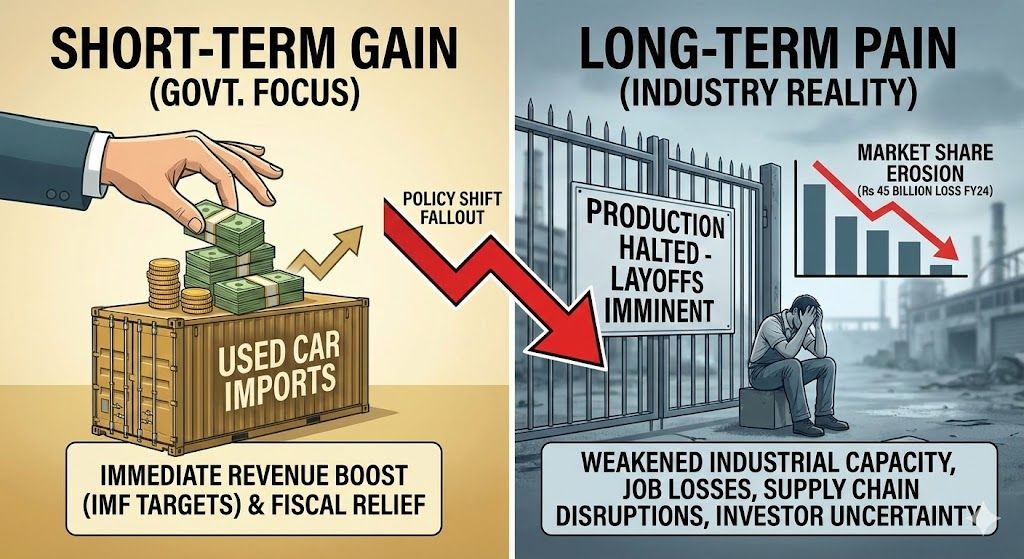

The biggest threat to the industry right now comes from the liberalisation of used-car imports. With the government under pressure to meet IMF targets and stabilise external accounts, the policy priority has shifted from strengthening industrial output to managing the balance of payments. As a result, trade and tariff structures are being realigned in ways that may unintentionally open the floodgates for used vehicles.

A 40% regulatory duty has already been introduced, but industry experts argue that gaps, cascading effects, and inconsistent enforcement could still allow imported used cars to flood the market — undermining locally produced vehicles in the process.

A Sector That Touches Millions

What makes this situation so concerning is the sheer size of the auto sector’s footprint in Pakistan’s economy. Around 2.5 million jobs are linked directly or indirectly to automobile production. Nearly 1,200 factories — from small-scale vendors to major component manufacturers — supply parts for locally assembled vehicles.

The industry contributes roughly PKR 700 billion in taxes, almost 6% of the government’s annual revenue. And localisation efforts save close to USD 1.5 billion every year through import substitution.

These aren’t just numbers — they represent families, factories, and entire communities that depend on the continuity of local car production.

What Happens If Local Manufacturing Shrinks?

If used-car imports rise unchecked, fewer vehicles will roll out of domestic assembly plants — and the first to suffer will be local parts vendors. Order volumes would shrink, leading to job losses and production downtime. Tax revenues would fall. And once the supply chain contracts, restarting it becomes extremely difficult.

This pattern isn’t unique to Pakistan. Even Germany, home to global auto giants, is now working aggressively to protect local manufacturers from Chinese EV competition. The global lesson is clear: strategic industries must be strengthened, not abandoned.

Short-Term Gains vs Long-Term Loss

Used cars do offer short-term relief for consumers looking for cheaper options. But Pakistan must decide whether short-term affordability is worth long-term industrial decline. If policy leans too heavily toward imports, automakers may eventually abandon assembly altogether — choosing instead to become importers themselves.

That would turn Pakistan back into a trading economy, not a producing one.

A Better Path Forward

A stable, forward-thinking policy framework could create room for both competition and industrial growth. A tariff differential of at least 40% between imported CBUs and locally assembled CKDs would give manufacturers the breathing space needed to survive and invest.

New EV players should be allowed in — but only with binding localisation requirements. They must begin local assembly within three years and gradually contribute to exports thereafter.

On the import side, Pakistan must enforce strict international standards:

– Pre-shipment inspection

– Road-worthiness certification

– Emissions compliance

– Crash-test verification

– Guaranteed spare parts availability for at least 10 years

Depreciation-based duties must be rationalised, and carbon/NEV levies should increase as imported vehicles age.

Reforms Are Needed — But So Is Stability

Protecting the industry doesn’t mean protecting inefficiency. Local automakers must improve safety standards, update models more regularly, and compete on merit. But they also need a predictable policy environment to do so.

A Make-or-Break Moment

Pakistan now faces a defining choice:

– Remain an assembly-and-import market, or

– Transform into a competitive manufacturing and export base.

The industry is ready for reform. The real question is whether policy will enable that reform — or unintentionally dismantle the foundation that took decades to build.

If policymakers choose wisely, the auto industry can still be one of Pakistan’s strongest growth engines. If they don’t, the loss of industrial capacity could be permanent — and once gone, it will be extremely difficult to rebuild.

The author is a communications expert and writes on the issues of public interest. His X handle is @khawar69 and he can be reached at khawarazhar@gmail.com.